Another definition of the upper class...

Making it all about the Benjamins

In my last post, I took Rob Henderson’s definition of the upper class from his book Troubled and tried to operationalize it around parental and personal educational attainment. While I find that definition reasonable, it has some practical challenges when it comes to examining the views of the upper class or comparing them to everyone else:

There’s just not a lot of good survey data that measures where respondents went to school (and whether their parents did), and

Per our comparison of editorial boards, I suspect (i.e., a few shades lighter than a proper hypothesis) that there is a left-wing tilt to that definition that colors all differences between the upper and lower class, so defined.

But recall that Henderson’s original definition of luxury beliefs said that luxury beliefs:

are ideas and opinions that confer status on the rich [emphasis added] at very little cost, while taking a toll on the lower class.

So I’m going to back away from the “upper class” (which only later gets defined in terms of education anyway) and ask: who are the rich?

I don’t know about others, but when I imagine the rich, I imagine people who have substantial monetary resources to the point where they can live basically indefinitely without having to work.

And I’m here to tell you: I think that’s an unreasonable definition. It has too many imprecise words: substantial, basically, indefinitely. I don’t see how we get anywhere with my imagination.

Instead, I think we need to start from a crowdsourced concept of rich. That is: what, on average, do our fellow Americans think rich means?1 And for that, we have to ask: rich in income, or rich in wealth?

The Rich by Income

Now, properly speaking, “wealth” is really something like “net worth”, or assets less liabilities. In everyday language, though, we often refer to “rich people” as people with high incomes. That’s a little sloppy and imprecise of us, but since we’re crowdsourcing here, let’s not judge the crowd (just yet). What do we call rich?

For the last two years, Bankrate asked U.S. residents what it takes to be rich. Here’s what we said in 2024:

Yes, you read that correctly: Americans think they’d need an annual income of $520,000 to feel financially free or rich. I’m not sure whether that’s individual, household, or family, but no matter how you slice it, that’s a pretty narrow cut of the income distribution in a country where the median annual wage is less than $50,000. By one estimate, such an income puts a household solidly at the 98th percentile of the income distribution last year.

Henderson and the rest of us combined appear to get to a similar place by very different means: “the rich” are a small group of just a couple percent of the population. Whether we use his cultural definition based on parental and personal education or a hard income cutoff, the rich is a pretty narrow slice of the pie.

But maybe “the rich” and “the upper class” aren’t the same group? Or, if you will, perhaps the rich are a subset of the upper class? In the same survey, Bankrate also asked what annual income one would need to feel financially secure or comfortable. And here’s what we said:

On average, Americans felt an annual income of $186,000 in 2024 would make them financially secure. You may argue that financially secure does not mean upper class, but rather middle class, but, I mean… c’mon. Are we really going to claim that an income that’s more than double the highest median household income ever in the U.S. is as middle class as the actual middle income? Like, really?

{kind=link}

Let’s hold there for a second and pivot to wealth.

The Rich by Wealth

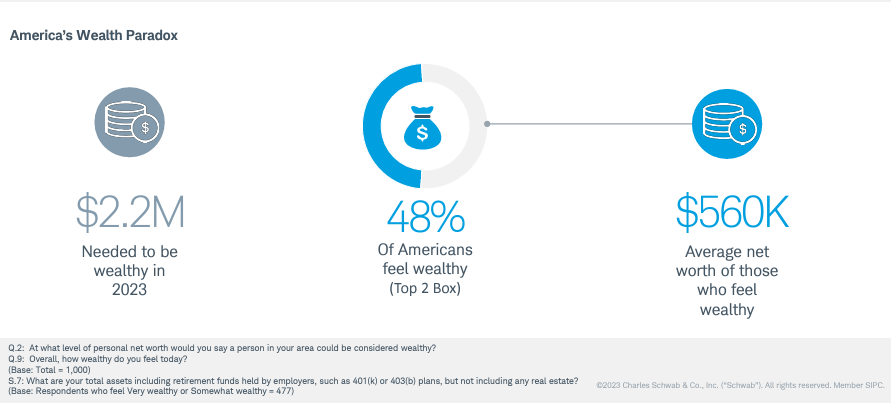

As it happens, Charles Schwab asked U.S. residents just last year (2023) what it takes to be wealthy.2 And they answered: averaged across all respondents, it takes a net worth (total assets less total liabilities) of $2.2 million. Around the same time, the Federal Reserve ran the latest wave of the Survey of Consumer Finances, which among other things allows us to calculate the distribution of net worth of households in the U.S. It turns out DQYDJ created a calculator to help us find what percentile of the net worth distribution any level of wealth is. Here’s $2.2 million:

A (household) net worth of $2.2 million puts one at the 91 percentile of the wealth distribution in the U.S.3 So one way of thinking about this is that about 9 percent of the households in the U.S. are in the upper class. That’s a little less than our “financially secure” group, but several times more rich people than our “rich” income cutoff.4

And yet… in the same survey, Charles Schwab also found this:

That’s right: when asked what net worth someone would need to be wealthy today, the average answer was $2.2 million, which about 9 percent of U.S. households possess. But in the same survey, when asked whether people feel wealthy, nearly half of respondents said “yes!”, and those people had an average net worth about 75 percent less than the amount needed to be wealthy. Indeed, if we take the average net worth of those who said they were wealthy as the lower bound of “rich”, then households above the 72nd percentile of net worth are rich.

And not to put too fine a point on it, but that’s a lot more people than attended selective colleges. Indeed, that’s almost as many people as have a college or postgraduate degree in the U.S. at all.5

The Bottom Line

Here’s where I get all squishy. I’m not saying that using (almost) the top 30 percent of the population defined by net worth to define rich is wrong. It strikes me as a reasonable definition given people’s views on the matter. I am saying that it seems inconsistent with other responses people give on the issue, including either measure of income we use to define “rich”, “financially secure”, or “upper class.”6

But using the “financially secure” cutoff for rich, while failing to capture my personal imagination, seems more reasonable to me. Using a household income cutoff (maybe adjusted for household members, where available?) identifies a group of households that’s a little more than 10 percent of the population. They have substantially more means than most of the rest of the country (and remember that even the bottom two quintiles in the U.S. have substantially more than the rest of the world!).

So going forward, when I can find data that splits out views by income, a cutoff near this number is… perfectly reasonable for my purposes. Whether it’s a hard numerical cutoff or “about 10 percent of the respondents by income” when the sample is all households, that’s going to be our ongoing definition of the upper class.

And for your more globally or historically minded folks: yes, at some point (in another essay) I’ll get to that, too. I think it is uncontroversial for me to say this here, though: by both global and historical standards, a very sizable chunk of U.S. residents are rich. Probably more than half. But again, we’ll come back to that.

The exact question wording was “at what level of personal net worth would you say a person in your area could be considered wealthy?” So note that I’m pulling a little sleight of hand here between wealthy and rich, and also between personal and household. I am uncertain to what degree respondents made the same substitutions.

I don’t know what that is worldwide, but it wouldn’t surprise me if it were 98th or 99th percentile.

And, of course, these are not all the same people. I keep using these comparisons of the percentage of the population for those of you who are hard-core relativists, and think of the rich as some fixed percentage of the distribution irrespective of their absolute material means.

And it gets better! There’s several pages of response data in the attached document where people really define being wealthy in terms of having time. I can’t decide whether this is genuine and people are really valuing “what matters in life”, or this is a form of coping since average work hours have fallen a goodly bit since World War II (and even more since the 1800s).

That said, a recurring theme of this Substack will be that people’s views on many issues are wildly inconsistent. So maybe that’s a feature of this cutoff, not a bug?

🙋♀️ question. Why do we think Black Americans need nearly 100k more to feel financially comfortable/secure?